Planning a shopping spree in Asia? Here's some exciting news that'll make your wallet happy! RuPay has launched an incredible cashback offer that lets you save big while shopping across four major Asian destinations: Japan, Singapore, Indonesia, and Philippines.

Flat 25% cashback on all Point-of-Sale transactions

Maximum cashback: ₹3,000 per transaction

Valid in: Japan, Singapore, Indonesia, and Philippines

Campaign period: October 30, 2024 - January 29, 2025

Total cashback limit: ₹15,000 per card

Looking for a great card to get started? Consider the IndusInd Bank Platinum RuPay Credit Card - it's lifetime free and offers 0.7% cashback on UPI transactions with quick approval process.

Remember that incomplete, declined, or disputed transactions won't qualify for the cashback. The offer is non-transferable, and NPCI reserves the right to modify or discontinue the campaign. Any issues with merchants need to be resolved directly with them.

This offer will be fulfilled by individual banks - you might need to chase your bank to realize the rewards if they do not credit them automatically.

This winter, make your Asian shopping adventure more rewarding with RuPay JCB Credit Cards. Happy shopping!

We've all seen those Instagram posts – someone flashing their shiny American Express card at a premium restaurant, or humble-bragging about their airport lounge access. We've watched endless Twitter threads breaking down "🔥How I Turned a 8 Lakh Spend on My AMEX Card into a Dream Vacation🌟

Hello from mountains" and "How I maximized my Amex points" – usually ending with a not-so-subtle referral link. But there's another reason you're seeing so many Amex recommendations lately: lucrative referral bonuses.

The Referral Trap

Amex offers some of the most generous referral bonuses in India:

Up to 25,000 reward points per referral for Platinum card holders

Up to 8,000 reward points for other cards

Multiple referrals allowed per year

This creates a perverse incentive where cardholders aggressively promote Amex cards on social media and to friends, often downplaying the cards' limitations while highlighting only the benefits. Remember: the person referring you stands to gain significantly from your sign-up. If you think you need an Amex, you should do it from a referral anyway though, as you stand to benefit from it as well.

The Fear of Missing Out (FOMO) around Amex cards in India is real, amplified by both social media showoffs and these referral incentives. But before you jump on the bandwagon, let's understand why getting an Amex card just because everyone else has one (or because someone is pushing you to use their referral) might not be the smartest financial move.

Let's address one of Amex's genuine strengths first: their rewards program, particularly for air miles, is legitimately excellent. The earn rates are competitive, the transfer partners are solid, and for the right user, the value can be substantial. However – and this is the crucial part – whether this translates into real value depends entirely on your usage patterns and redemption choices.

Excellent transfer value for Marriott Bonvoy, Taj, and international airline programmes

Amex can also give a return of as much as 6.66% (for Amex Gold; this becomes 4.67% for MRCC and 3.5% for Platinum Travel ) back in cash for buying vouchers for Amazon, Flipkart etc. - if you do not have a better card for this, go for Amex by all means (we have used referral links - not being a hypocrite, but it helps the person getting the card too).

If not, here's where you need to be honest with yourself. While the points are valuable, the practical redemption options within India are more limited than they appear:

Primary valuable redemption within India is for Marriott properties

Most Marriott hotels in India are luxury properties (₹15,000 to ₹40,000+ per night)

Limited mid-range redemption options within India

Need to plan international travel to maximize value from airline partners

It is important to introspect whether you really need an Amex:

Reality Check Questions

Before jumping in, ask yourself:

Do you regularly stay at luxury hotels?

Are you planning international travel where these points have more value?

Will you actually redeem points, or will they sit unused?

Is your spending high enough to accumulate meaningful rewards?

Are you disciplined about maximizing point values?

FOMO is a powerful motivator, but it's a poor basis for financial decisions. Instead of following the crowd:

Amex is great when used right

Analyze your spending patterns

Calculate the real cost vs. benefits using the redemption rates above

Consider your local market's acceptance rate

Choose a card that truly serves your needs, not your social media feed

Key Takeaway

Remember, the most impressive financial decision is often the one that makes the most practical sense for your situation, not the one that looks best in your wallet. If you're primarily interested in travel rewards, consider cards that offer more flexible redemption options within India's travel ecosystem.

🔥 LIMITED TIME OFFER: Get 10% bonus Club ITC points when transferring from Axis Bank until November 15! Check offer details here

Are you sitting on a pile of Axis Bank reward points wondering how to make the most of them? Here's a detailed guide on how you can convert those points into domestic travel bookings through Club ITC and International Travel House (ITH).

International Travel House vouchers can be used for:

Domestic flights and trains

International flights and trains

Hotel bookings

Airport transfers

Visa services

It's recommended to compare ITH rates with other booking options before redemption - while rates are generally competitive in my personal experience with online travel agencies (OTAs) and direct bookings, it's always good to verify.

With the current 10% bonus offer, now is an excellent time to convert your Axis Bank reward points to Club ITC points. While the voucher redemption process involves a few steps, the competitive rates and flexibility in booking options make it a worthwhile redemption choice for your reward points.

TLDR: Limited details added so far with no information on value of each chip. Scroll for our recommendations for best credit cards for Indigo

IndiGo's new frequent flyer program, IndiGo BluChip, allows members to earn BluChips on every IndiGo flight across both domestic and international routes. Members earn 8 BluChips for every INR 100 spent, with bonus points for higher-tier members (Blu 1 earns an additional 4 BluChips/INR 100; Blu 2 earns 2 extra BluChips/INR 100). Booking through IndiGo's website or mobile app also provides a Channel Bonus of 4 BluChips/INR 100. Passengers can retroactively claim BluChips within 90 days of a flight, provided they update their membership number.

In addition to flights, members can earn BluChips on select 6E Add-ons, such as excess baggage, seat selection, and priority check-in. Like flight bookings, these add-ons also provide 8 BluChips/INR 100 with potential bonus points for Elite members. BluChips can be redeemed for any IndiGo flight (economy or Stretch class), with no blackout dates or seat restrictions, but cannot be used for add-ons, taxes, or fees.

Indigo has not declared any additional miles earnings for their existing co-branded card offerings (both the Kotak and HDFC cards don't offer great value, and Kotak isn't even allowed to issued cards as this was written).

Axis Atlas becomes an even better choice for Indigo as one gets 50% bonus BluChips for booking directly on Indigo website / app. Click here to apply!

All other cards from our flights section should be very useful as well, given that Indigo does award BluChips for bookings through platforms / OTAs

As a young adult in India, getting your first credit card can be an exciting step towards financial independence. However, it's essential to approach this milestone with caution and wisdom. Here are five valuable tips to help you navigate the world of credit cards:

1. Explore Special Offers: Leverage Your Connections

There are several avenues to explore for special credit card offers:

Many banks offer special credit card deals to recent graduates. These cards often come with the attractive benefit of a Lifetime Free (LTF) feature, meaning you won't have to pay annual fees. Some notable alumni offers include:

ICICI Bank Sapphiro Card

HDFC Bank Diners Black Card

SBI Card ELITE

SBI Card AURUM

Check with your college alumni association or directly with these banks to see if you qualify for these premium cards with special terms for alumni.

If you're employed, your company might have partnerships with certain banks, offering preferential rates or benefits on credit cards. Some banks known for strong corporate partnerships include:

HDFC Bank

Axis Bank

AU Small Finance Bank

Check with your HR department about any such tie-ups your company may have. Don't hesitate to shop around and compare offers from different banks based on your alumni status, employer, or existing banking relationships.

If you have a salary account with a bank, you're already a step ahead. Banks are more likely to approve credit card applications from existing customers, especially those with regular income. Plus, having your credit card and salary account with the same bank can make managing your finances much easier.

For example, IDFC First Bank is known to provide credit cards to their salary account customers, often with favorable terms. Many other banks also offer preferential treatment to their salary account holders when it comes to credit card applications.

3. Start Small: Don't Chase Premium Cards Right Away

It's tempting to go for the most prestigious card with the best rewards, but as a first-time applicant, you might not qualify for these. Instead, focus on getting approved for a basic card. Remember, building a good credit history is more important than having a fancy card in your wallet. Be patient and work your way up to better cards over time.

These products mix credit and investments, which can be tricky:

Your credit limit is tied to your investments, making it hard to access funds when needed.

They often have complex terms that are hard to understand.

You might be forced to sell investments at a loss if you can't repay your credit card debt.

It's easy to take on more risk than you're comfortable with.

Instead, keep it simple. Use your credit card responsibly and keep your investments separate. This approach gives you better control over your finances and reduces risks.

Remember, a credit card is a tool for building credit history and managing short-term expenses, not free money. By following these tips and avoiding risky products, you'll be on track for a healthy financial future. Happy responsible spending!

As someone who's always on the lookout for ways to optimize my spending, there is an underrated gem in the HSBC Live+ Credit Card (previously known as HSBC Cashback card, which I have held for a while). It is my go-to card for a significant portion of my offline expenses, and for good reason.

The standout feature of this card is its impressive 10% cashback on dining and groceries. These categories make up a large chunk of my monthly budget when it comes to spends at physical stores, so the savings really add up. Whether I'm grabbing a quick bite or doing my weekly grocery run, I know I'm getting substantial value back on every purchase. A nice supplementary benefit is a 20% discount on Myntra on orders above Rs. 3,000

The card gives cashback on any amount that you spend - unlike say a Diners Black that gives points for every 150 rupees. We have written a data-driven report about how important this efficiency is, which you can find in our slippage and vouchers guide.

Unlike some rewards cards that require you to jump through hoops to redeem your points or miles, the HSBC Live+ keeps it simple. The cashback is automatically adjusted against your next statement. No need to track points or worry about expiration dates – your savings are applied effortlessly.

New cardholders can take advantage of an attractive welcome offer - where you get an extra Rs. 1,000 cashback for a spend of Rs 20,000. Even better, this offer extends to addon cards as well - so whenever you get an addon card - you can get an extra Rs. 1,000 for every Rs. 20,000 spent on the card. This is a great double dip opportunity. Overall, this makes it an excellent choice for families looking to maximize their rewards across multiple spenders.

You also get a Rs. 250 voucher for a successful vKYC

If you're interested in adding this powerful cashback tool to your wallet, you can apply here and get Rs. 750 Amazon Pay voucher extra (+ Rs. 250 Apay voucher on vKYC). Full disclosure: This is an affiliate link, and using it helps support the running of this blog. We appreciate your support in keeping our content free and accessible!

The HSBC Live+ Credit Card has become an integral part of my financial strategy, offering substantial returns on everyday spending with minimal hassle. If you're looking to optimize your credit card rewards, especially on dining and groceries, this card is definitely worth considering.

With recent changes, two great options for earning rewards on tax payments are the Amex Platinum Travel Card and the Amex MRCC (Membership Rewards Credit Card).

Important Notes:

The HDFC BizBlack Card, while being more rewarding, is exclusively available to business owners.

Tax payments can be made through the Canara Bank portal, which charges a 1% convenience fee for credit card transactions.

Amex does not give regular RPs for paying taxes, but does give milestone benefits

Both cards have healthy welcome offer currently through referrals. Platinum Travel is great for a 4L liability - it has a better welcome offer and a Taj voucher too. Else, MRCC can work out better (or both!)

There are a few other cards that can work okay (Emeralde Private Metal, HSBC Premier), but they are harder to get and have lower rewards.

Most cards out there have a very standard reward structure: something on the lines of 6 points for every ₹200 (called quantum henceforth) spent. While this might give an enticing rate of 3% returns, the actual return that we get can often be much lower. For instance, let's assume that we spend ₹250 on a transaction - the actual reward rate is 6/250 = 2.4% and not 3.0% . This loss of 0.6% is defined as slippage.

I compiled together all transactions I made on taxi apps over the last 4 years, and simulated the effective reward rate for a set of cards (ones that I own mostly)

Card

Quantum

Points per Quantum

Actual Reward Rate

Slippage

Diners Black

₹150

5

2.54%

0.79%

Axis Atlas

₹100

4

3.36%

0.64%

Magnus

₹200

9.6

2.92%

1.88%

Vistara Ultimate

₹200

6 + (4.8 towards milestone)

4.23%

1.17%

Max(above)

N/A

N/A

4.37%

N/A

Magnus (with monthly 1L spend)

₹150

9.6 + 20 towards milestone

22.92%

1.88%

From this analysis, there are a couple of major takeaways:

Cards with milestone benefits don't suffer from slippage, as any amount that is spent counts towards the milestone. This shows up in the great rate for Axis Vistara Infinite, but even more so on the Magnus assuming a monthly 1L spend. Amex Platinum travel is another great card with milestone bonuses that works well this way

The smaller the quantum, the better is the reward rate in general; this shows up in Axis Atlas, which doesn't suffer as much relatively due to a quantum of ₹ 100

Choosing the card depending on transaction value can get you a small gain in the overall efficiency.

Vouchers for a number of brands can be purchased online, that let you load up a wallet towards future purchases. Some of these include the Gyftr portal for HDFC, Axis, SBI, StanC etc. , direct vendor websites (eg: Uber), Amazon gift card store, MagicPin, NearBuy etc. vouchers are mostly immune to slippage - except for the initial transaction used to buy the card. Using our earlier example of 6 points for ₹200 - if we buy a voucher for ₹2500, we get an effective reward rate of 2.88%, which is a lot closer to the ideal 3%. Furthermore, a lot of these portals give out vouchers at an additional discount (eg: 5X points for SmartBuy Infinia / Magnus at the time of writing), which brings the overall reward rate even higher! Keep an eye on the Technofino community for good offers on cards

There are a couple of things to be careful with vouchers:

Ensure you read the terms and conditions - specifically around whether a voucher may be split across multiple transactions, and how many vouchers may be used for a single transaction.

Buy only what you need - vouchers have an expiration date; ensure that you buy what you need, and keep track of your vouchers

Vistara has the by far the most rewarding frequent flyer program in India, with great co-branded cards. This post listsf steps towards maximizing the value you can get with Vistara

Please see the destinations page to see if Vistara works for you

Vistara has co-branded credit cards with Axis, SBI and IndusInd banks. The main benefits from the cards are:

Free flight ticket vouchers on signing up, and hitting milestones

Club Vistara membership and tier upgrades

Card

CV Tier

Joining / Renewal Fees

Points /₹200

Ticket

Milestones

CV SBI

Basic

₹1500 / ₹1500

3

ECONOMY

₹1.25L,₹2.5L,₹5L

Axis Vistara

Basic

₹1500 / ₹1500

2

ECONOMY

₹1.25L,₹2.5L,₹6L

CV SBI Card PRIME

Silver

₹3000 / ₹3000

4

PREMIUM

₹1.5L,₹3L,₹4.5L,₹8L

Axis Vistara Signature

Silver

₹3000 / ₹3000

4

PREMIUM

₹1.5L,₹3L,₹4.5L,₹9L

Axis Vistara Infinite

Gold

₹10000 / ₹10000

6

BUSINESS

₹2.5L,₹5L,₹7.5L,₹12L

IndusInd Bank Explorer

Gold for 1st year

₹40000 / ₹10000

8 - Vistara, 6 - Hotel / travel. 2/1 - others

BUSINESS ( 1st yr only )

₹3L,₹6L,₹9L,₹12L,₹15L

Cards have offers for bonus CV points for spend milestones in 90 days in the first year. There are a few more benefits, that I have left out. In my personal opinion, Economy vs Premium doesn’t make a big difference on lower durations. Further, the high joining fee for IndusInd does not justify the returns in my opinion.

Taking these into account, below is a comparative analysis of the different co-branded cards (skipping IndusInd Explorer). For the analysis, we make the following assumptions:

Value of 1 CV Point = ₹1. Upgrade voucher = ₹1000. GST of 18%

1 economy/premium ticket = ₹5000, 1 business ticket = ₹6000. You may value it higher, but I don’t think its worth it

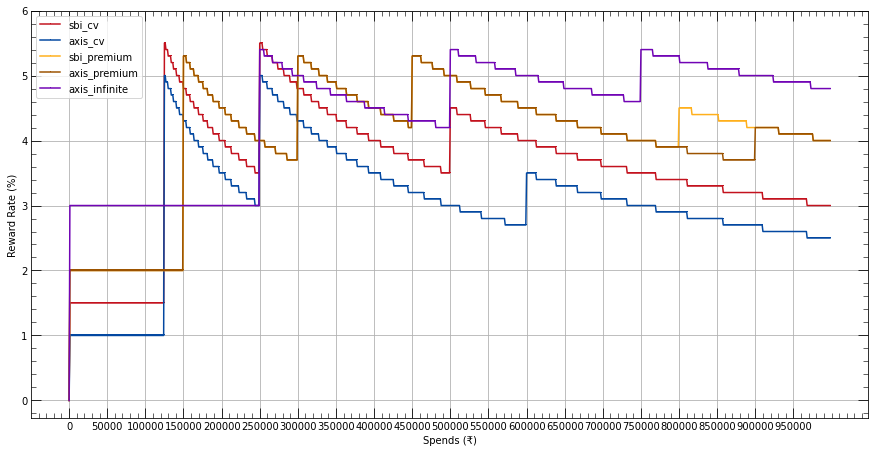

The chart below shows the rewards vs spends - the joining/renewal fees are accounted

From the chart, we can get the following inferences:

CV SBI / Axis Vistara give the best net returns until a spend of ₹3L, followed by CV SBI Premium / Axis Vistara Premium until spends of ₹7.5L

I also hold Axis Vistara Infinite - largely for priority checkin, boarding and baggage - I personally find it valuable

Looking at the strict reward rate (not taking joining fees, joining bonus and upgrade vouchers into account) below:

The 5.x % reward rates at milestones is better than what one can earn on most cards for general spends. This makes for a compelling case for using the CV cards as the default credit card for all spends except where multiplier offers give a better return. These multiplier offers form the final piece of the reward point jigsaw and are discussed in the next section. My personal recommendation would be to get a basic SBI ClubVistara card for the insane rewards, and the Axis Vistara Infinite card for Vistara gold benefits

This section gathers together some great offers on other cards for specific spends, which can give a huge number of CV points in return. It is important here not to spend for the sake of spending 🙂

Atlas has a base reward rate of 4 CV points for every ₹100 spend, and 10CV points for every ₹100 spent on travel (flights and hotels) on Axis Bank’s portal. The CV account further adds on 8 - 11 CV points (depending on tier) if the card is used to book a Vistara flight: giving a net 18 - 21 CV points on Vistara, and 10CV points for other airlines/hotels. Further, for a joining fee of ₹5000, 10000 (minimum 5000 from year 2) CV points are obtained as a welcome bonus, so it makes sense to get this card just for the first year bonus.

Atlas has a base reward rate of 4.8 CV points for every ₹100 spend, and 24CV points for every ₹100 spent on travel (flights and hotels) on Axis Bank’s portal, giving an insane 32-35CV per ₹100 spent on Vistara flights, and 24CV per ₹100 on hotels and other airlines. Further, Axis edge portal can have some great multiplier deals upto 8000 CV points per month, and the gift-edge portal may be used to purchase vouchers at 5X and 10X points - including vouchers from AmazonPay etc. On top of this, hitting a monthly spend of ₹100000 will net you 20000 CV miles on top of everything else, so if you’re anticipating a month with high spendings, Magnus should become the default card for all purchases hands down!

Both of these currently have a base reward rate of 3.33 points (1 HDFC point converts to 1 CV point) for every ₹100 spend, and 20 points for every ₹100 spent on travel. HDFC SmartBuy also has some nice deals on railway tickets (10CV points per ₹100), and gift vouchers (17.5 CV for Infinia, 10CV for Diners - for ₹100 spends). These can be a great complement to the Axis cards - SmartBuy points give you the flexibility to redeem on all airlines

Overall, I will recommend going for all of these - they can take your miles game to an insane new level. Infinia is generally hard to get, and Atlas may be used for the first year if you get a Magnus too